Buy a car you can actually afford with these tips

Table of Contents Setting a monthly numberCalculating the monthly paymentOther things to consider Read through

Table of Contents

Read through our tips and advice before taking those new car keys.

Thianchai sitthikongsak/Getty Images

Buying a new car is a massive purchase. Aside from a house, it’s perhaps one of the largest purchases anyone makes in their life and car payments are a big financial responsibility. Keeping with the house purchase metaphor, you want to make sure you buy a new car that’s within your budget. Yes, that may mean skipping out on something fancier or foregoing the latest features, but keeping things financially responsible is always good.

Of course, knowing a car’s full list price isn’t necessarily that helpful to figuring out whether you can afford it. Most of us plan our budgets monthly and thus want to know how much the payments for a new car will cost each month. Here are some guidelines to help you find a reasonable figure. Read on for our tips and advice to make sure you don’t overspend on a new or used car. That way, when you sign the papers, you can drive home with your new car knowing you made the best decision possible.

Setting a monthly number

It might seem obvious, but the first step to figuring out how much you can spend on your new car is to calculate your monthly budget. Add up all your monthly income, subtract expenses (everything from rent or mortgage payments to food and healthcare), and see how much is left over. For your benefit, the Federal Trade Commission even offers a sample budget sheet online.

But don’t dedicate very last penny of disposable income to a car. Instead experts have developed some guiding rules for how much is reasonable to spend.

In the past, advisers sometimes recommended what was called the 20/4/10 rule: make a 20-percent down payment, have a loan lasting no longer than four years and don’t let payments exceed 10 percent of your gross income. But those figures just aren’t realistic for today’s shoppers. In part that’s because car loans last much longer: In March 2020, the average auto loan surpassed 70 months, according to Edmunds research.

Today, experts generally recommend spending no more than 15 percent of your monthly take-home pay (that’s how much you receive after taxes and other deductions). Depending on your budget, spending closer to 10 percent might be a more reasonable guideline.

Based on those rules, somebody with a take-home income of $3,000 per month might consider a payment of $300 to $450 per month, figures that represent 10 and 15 percent of their take-home pay, respectively. If you’re not looking at a fancy SUV or pickup truck, that’s generally a good number when shopping more affordable new cars.

However, it’s important to note that you’re responsible for more than just the car payment. Factor in insurance costs, too, when figuring out your total monthly car expenditure. Don’t let the combined cost of insurance and the car’s payment exceed the rule you’ve set for yourself, whether that’s 15 percent or some other value. For that reason, picking a base car payment closer to 10 to 15 percent of your take-home income is a safer rule to ensure you won’t blow your budget.

For this reason, many advisers instead recommend setting a limit for how much your total car expenses will be per month. For instance, you might decide to spend no more than 15 percent of your total take-home pay on your loan payment, insurance and gas costs combined. That can be an especially important rule for buyers who already have other debts.

Your monthly payment can vary significantly depending on your credit score, the length of your loan and the size of your down payment.

Audi

Calculating the monthly payment

Once you know how much you can afford to spend, it’s time to work out how much you’d pay for the car you want. New car ads and review sites generally list only the total MSRP (manufacturer’s suggested retail price), so you’ll need to convert that to a monthly figure. Most carmakers offer a loan calculator on their consumer websites. Simply input data like your potential down payment and interest rate, and the site’s calculator will tell you approximately how much the loan would cost per month.

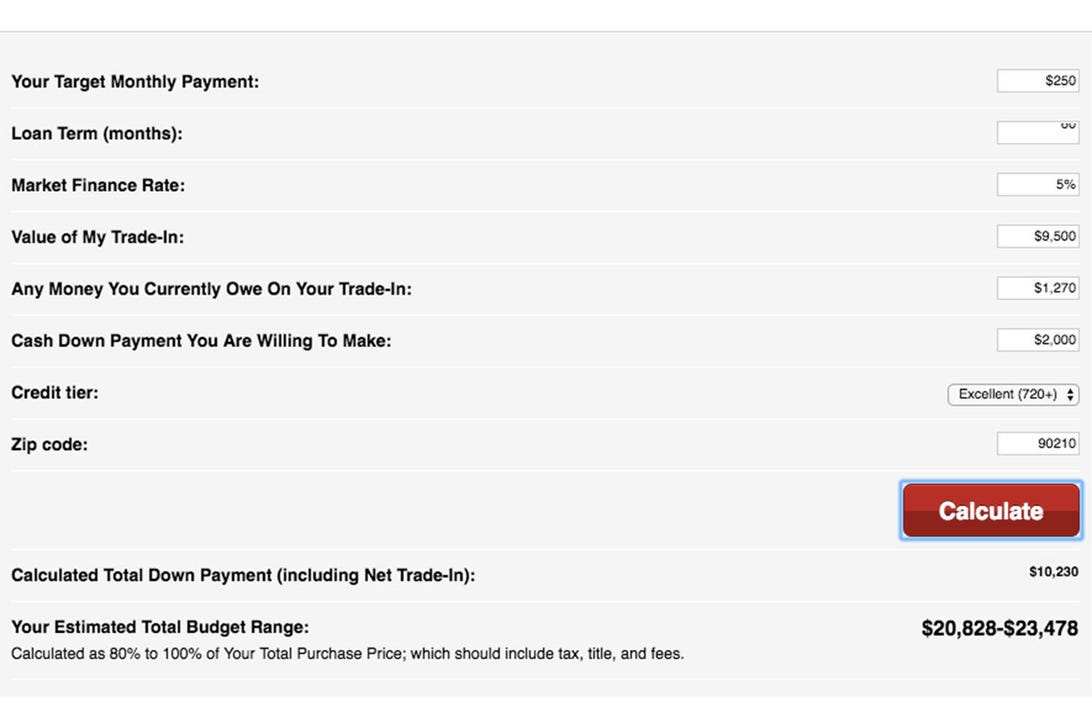

We’ve also got a loan calculator available within the Roadshow website. Enter how much you want to pay per month, as well as details like your expected loan length, interest rate and other details, and our calculator will help you figure out how much car you can afford to buy. You can also go the other way with our basic loan calculator, inputting a car’s sale price and other data to figure an approximate monthly payment number.

Bear in mind that interest rates will vary considerably based on your credit history, down payment, and whether you finance through a carmaker directly, or through your bank or credit union. Rates remain generally low right now, but obviously, this can vary significantly from person to person.

You can use online calculators like this one from Roadshow to get an idea of how much you can spend per month.

Jake Holmes/Roadshow

Other things to consider

There are more costs to owning a car than just the payment and insurance. You should also budget for how much you’ll need to spend on gas and maintenance — although a new car should be covered under warranty for most of a new-car loan period.

Also consider the length of your car loan. While longer loans will, in general, give you a lower monthly payment, you’ll be paying more overall in interest charges. In addition, longer loans increase the amount of time you’re “underwater” on the new car. That’s the situation, known more formally as negative equity, when you owe more on your loan than the car is worth if it was sold. And that can make it more difficult to sell or trade-in the car.

Finally, don’t forget that these guidelines can and should vary depending on your situation. If you don’t drive very much, or spend a lot of your income on housing costs, you may prefer to spend less per month on your new car. If you’re a car enthusiast, or need a very specific vehicle for your job or commute, you might want to stretch your budget a little higher. Overall for most people, spending 10 to 15 percent of your monthly take-home pay on a new car loan is a good guideline.